Mike Smitka

Well, I've gone through another week without a post on the auto industry, but Thursday has come and my WREL Lexington (VA) radio segment with it. Here's my latest.

First, our host Jim Bresnahan asks about the gyrations of global stock markets. China? – attributing a reason to what happens in the stock market is hard. As an economist I don't pay attention to the stock market, because how it does has no link to the economy in the short run, and little or no impact on the economy. Most trading now is computer to computer, operating faster than the blink of an eye, and opaque in details. So why things move in a particular direction, and how much, no one can explain. Now the reporter on CNN has to give a report every hour, and we as humans like things to have causes, and they'll attribute the up or down to something. So in the short run the market is random, and betting on it is a crap shoot, one where the house – Wall Street – wins. You have to pay a fee, and the computers can see your trade before it gets executed and (legally – there's no regulation) bet against you. As to the US, we're seen a strong rise in the market the past few years have seen; the US economy has after all been growing, and corporate profits are up. Stock prices ought to reflect that, but the link is loose so things will go up and down. Don't panic, invest for that long-run link and don't let yourself try to beat the house in the short run.

Now as to China as a cause of the gyrations, what's been happening in China is not news. Of course I'm better informed than average. I've been teaching a course on the Chinese economy since I came to Washington and Lee almost 30 years ago, and first studied China when I was a freshman in college, over 40 years ago. I can read Chinese, albeit slowly and speak a bit. There are a couple historians in town, and literature and language specialists, and I can't begin to compare to them. But in this area I really am the go-to person. So here's what I see.

That the economy there is slowing, well, it began slowing a couple years ago. Over time an economy can grow only as it has new inputs, capital, labor, technology. China's population is no longer growing – and in a few years will begin falling – and the working age population is already in decline. That's been offset by migration, people moving from farm to city, but that is coming to an end. Much of the countryside has emptied out, and in particular there are very few young people working as farmers. That's the labor side, clearly slowing.

Then there's capital. China is the size of the continental US, and has completed its expressway system, which is more extensive and of course in better shape than our interstate system. That created a lot of jobs, and as in the US, that sort of construction also generated a lot of corruption. (We've forgotten how bad things used to be here, as over time we developed systems to monitor public works, while politicians have developed alternative, and more reliable, sources of funding.) Anyway, lots of other infrastructure is now also in place, and while cities are still growing, even there housing is often ahead of demand. For other sorts of capital China has also built up their economy. There are three times more cell phone users in China than in the US, and so the market is no longer growing, and most of the phones are made inside China as well. A lot of computers are in place. So capital accumulation is naturally slowing.

Then there's technology, one measure of which is total factor productivity. China has learned how to assemble cars, and while most of the engineering took place in Detroit and Wolfsburg – General Motors and Volkswagen control the top brands – the factory end is now pretty sophisticated. Cell phones are assembled in China, and more and more of the chips are made there. The world's largest PC company, Lenovo, is Chinese, and their universities graduate a lot of electrical engineers. While Lenovo started out by buying IBM's PC business, they now have enough experience to continue pushing the business themselves. So while China will keep improving, they're well along the catch-up process and the easy gains have already been made.

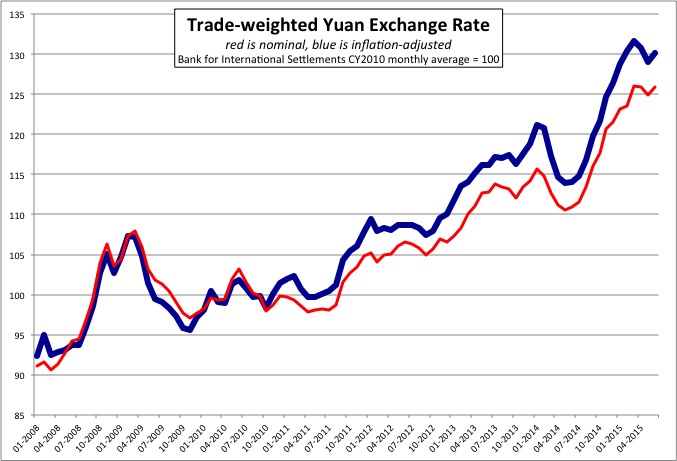

Hence China's headline growth has fallen from 10% to 7% and henceforth they'll slow to 4%-5%. That's still much faster than the 2% growth of the US. But as to the stock market, this slowdown was known to be happening, indeed was written about 20 years ago. The details of timing weren't know then, but the general outlines were clear. So what's happening in China isn't news and shouldn't have much effect.

Now there is the collapse in stock prices and some sectors of real estate. Chinese investors are not experienced, and many are naïve. In addition, for a variety of reasons Chinese bank accounts pay nothing. So as incomes have risen, money has flowed into stocks and real estate, and they've not been thinking carefully about long-run values. So there are a lot of empty apartments and people who have bought stock on the basis of rumors. While corporate accounting is much better, it's still weak – not that we don't have our scandals – so it's not always clear what you're buying. In any case, prices had no basis in reality and are now coming back to earth. Unfortunately it's very hard to work with that. Diagnosing a bubble is hard, and the tools that might pop it are also likely to trash the wider economy. So fighting a bubble can do more harm that good. But it's not clear why Wall Street should react strongly, since (unlike between Europe and Japan and the US) direct links between the financial system of China and those of other countries are weak.

Separately, there's a bit of news on the US end. Over the last 3 months housing prices have on average fallen a bit. Construction is back to growing on the pre-crash pace – but not at pre-crash levels. We're still down about a third – 31.6% to be precise – but there's no sign we're moving back towards prior levels. That's not good news. So while it's a backward-looking number, it will be interesting to see what we learn from today's release of GDP data.

Now we're about out of time today, but next week I want to talk about changes in the labor market at its two extremes, teens and older workers. During the Great Recession teen employment fell by one-third, but had been declining even before then. Are teens no longer interested in afterschool jobs? Or is there a lot of slack still, lots of people looking for jobs, and employers prefer to hire anyone but teens?

Then there's the older end. In 1981 only about 400,000 people aged 75 and above were working; today over 1.5 million older Americans are working. Some of that is simply that there are a lot more older Americans; our population is aging. But the share of older Americans working has also risen. So what's going on there?

More next week!